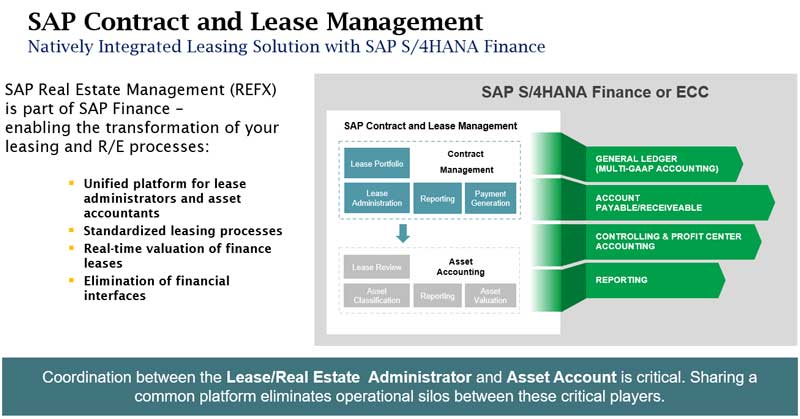

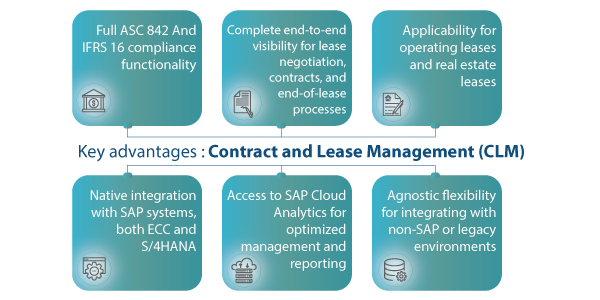

In 2018, the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) announced the release of new accounting standards, ASC 842 and IFRS 16, that redefined how organizations must account for leases.

These new leasing standards represent more than just an accounting change, with far-reaching and profound implications on lease/buy decisions, internal process coordination and financial reporting. Effective lease management must go beyond a one-time compliance perspective by enabling both ongoing management of lease changes and seamless integration with associated finance processes.