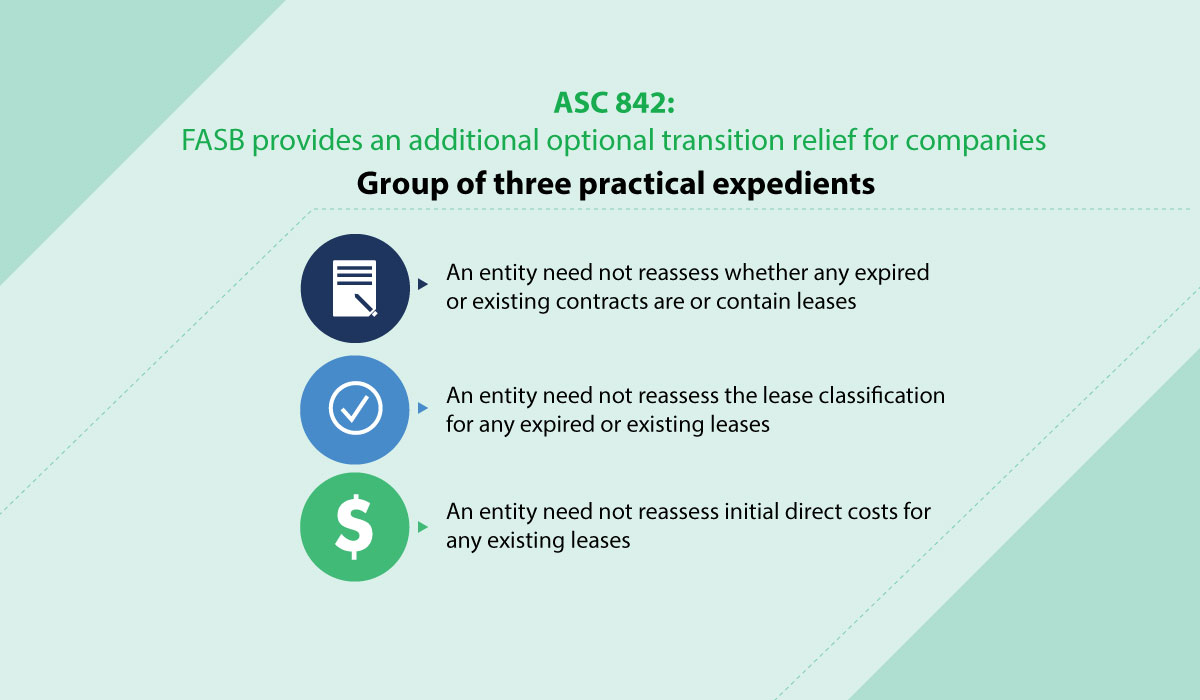

FASB has issued an update regarding ASC 842 through its Post-Implementation Review (PIR) process that is intended to respond to the concerns expressed by private company stakeholders about applying Topic 842 to related party arrangements between entities under common control.

Specific issues addressed in the PIR are:

- Which terms and conditions should be considered when determining whether a lease exists and, if so, the classification and accounting for the lease.

- The accounting for leasehold improvements associated with leases between entities under common control.