As a leader in compliance and finance innovation, Bramasol has introduced a new purpose-built CLM Rapid Solution that enables companies like you to quickly get up and running for ASC 842 or IFRS 16 compliance. It leverages the power of the industry’s leading leasing solution, SAP CLM, and combines it with Bramasol’s deep experience to provide a quick start that can get you up and running in 8 weeks instead of months or years and for a price that you can afford.

In this episode, John Scott, Senior Technical Accounting Adviser at Bramasol, shares insights of ASC 842 that applies to private companies and key issues that need to be addressed in order to succeed.

In February 2016, the Financial Accounting Standards Board

(FASB) issued Accounting Standards Update (ASU) 2016-02 (“ASC 842”) Leases, which provides new guidelines that change the accounting for leasing arrangements. The new leasing standard becomes effective in fiscal years beginning after December 15, 2018

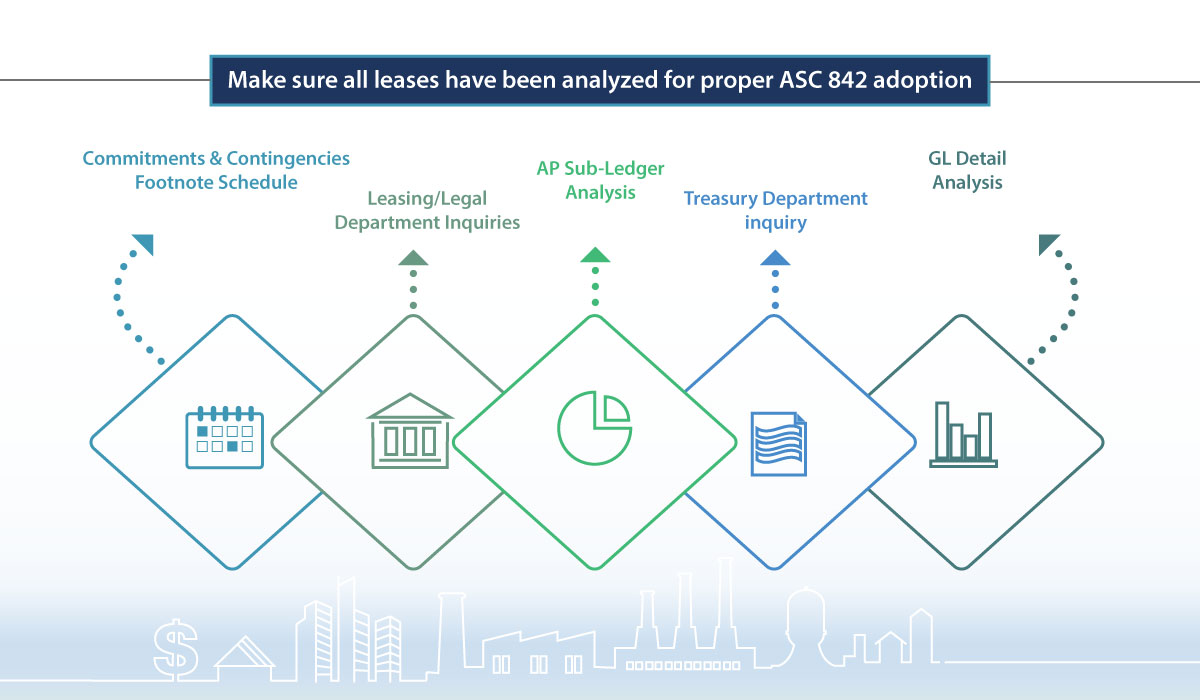

The new lease accounting standard ASC 842 is effective for public companies beginning January 1st, 2019. The primary purpose of the standard was to address the fact that most operating leases are deemed off balance sheet financing arrangements and currently are only disclosed via a company’s financial footnotes in the “Commitments and Contingencies” footnote.

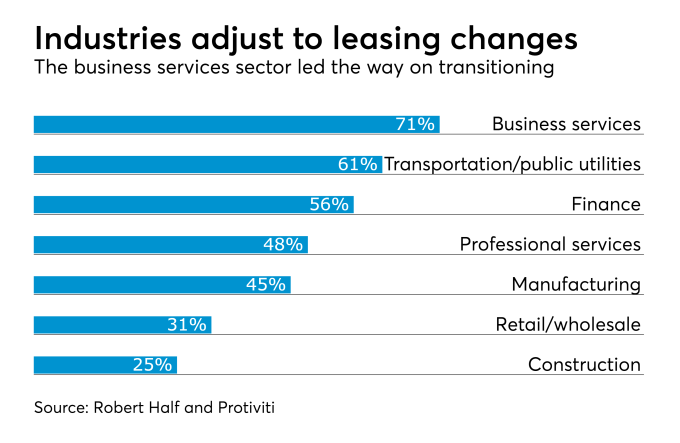

A recent article in Accounting Today provides an excellent view of how companies in many industries are moving toward compliance with the new lease accounting standards, ASC 842 and IFRS 16.

Nakisa, Bramasol's partner for leasing solutions, has announced general availability of the new 4.0 version of Lease Administration by Nakisa.

Bramasol, the leader in compliance and finance innovation solutions, has announced a new, purpose-built product that reduces complexity and implementation costs, to give companies across a variety of industries a ready-to-deploy solution for lease accounting disclosure reporting and compliance.

The customer is a Leading Global Organization and Multinational Retailing Corporation with annual revenues in excess of US$480 billion and which is one of the largest private employer in the world with over 2 million employees. As an international company, our customer is impacted by the new lease regulations ASC842 and IFRS16 that will take effect from January 2019.

In 2016, the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB) issued new standards for lease accounting: IFRS 16 & ASC 842, which must be implemented by 2019. Both IFRS 16 and ASC 842 are the result of a joint effort between the IASB and FASB to meet the objective of improved transparency, comparability and financial reporting. These changes will impact virtually all companies, whether lessors or lessees.