With the upcoming already extended deadline for the adoption of ASC 842, the new lease accounting standard in the US, many companies who have already adopted are struggling with managing the accounting under the new standard in spreadsheets or because they already chose a standalone software but are not happy with the results due to a lack of integration, causing reconciling issues or reporting inaccuracies.

According to the Big 4, over 50% of companies experienced a delay in compliance with ASC 606 and 842 due to accounting issues. Those same companies struggled to produce their disclosures and reporting. Underlying this are the technical accounting expertise and disciplines needed for success.

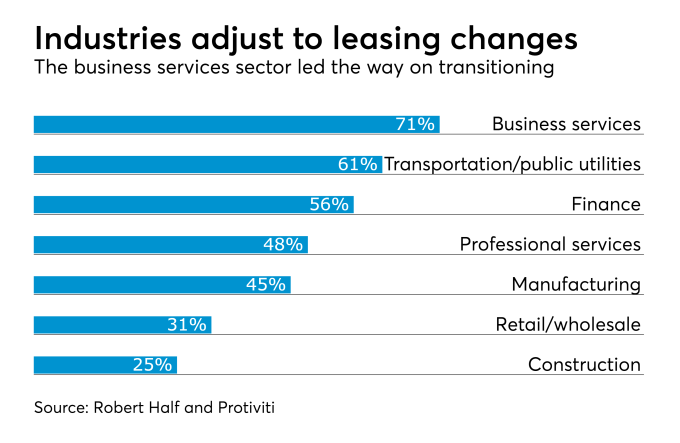

A recent article in Accounting Today provides an excellent view of how companies in many industries are moving toward compliance with the new lease accounting standards, ASC 842 and IFRS 16.

Nakisa, Bramasol's partner for leasing solutions, has announced general availability of the new 4.0 version of Lease Administration by Nakisa.

On January 5th, 2018, the Financial Accounting Standards Board (FASB) proposed adding an optional transition method and another practical expedient for lessors to Accounting Standards Codification (ASC) 842, Leases, to reduce the cost and complexity of implementing the new standard.

Bramasol, the leader in compliance and finance innovation solutions, has announced a new, purpose-built product that reduces complexity and implementation costs, to give companies across a variety of industries a ready-to-deploy solution for lease accounting disclosure reporting and compliance.

The customer is a Leading Global Organization and Multinational Retailing Corporation with annual revenues in excess of US$480 billion and which is one of the largest private employer in the world with over 2 million employees. As an international company, our customer is impacted by the new lease regulations ASC842 and IFRS16 that will take effect from January 2019.

In 2016, the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB) issued new standards for lease accounting: IFRS 16 & ASC 842, which must be implemented by 2019. Both IFRS 16 and ASC 842 are the result of a joint effort between the IASB and FASB to meet the objective of improved transparency, comparability and financial reporting. These changes will impact virtually all companies, whether lessors or lessees.